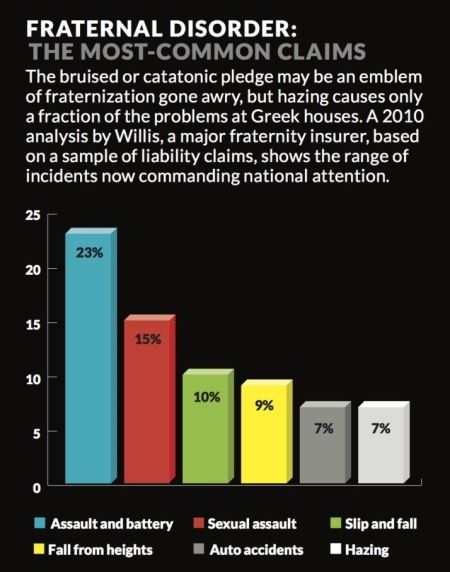

While the evils of hazing rituals at college fraternities are well known, the overwhelming majority of injuries suffered at college fraternity houses are not related to hazing at all. In a 2010 analysis of lawsuits related to injuries at fraternities performed by Willis, a major insurer for fraternities and sororities, hazing accounted for a relatively small 7% of injury-related lawsuits. Topping the list were assault and battery, sexual assault, slip and fall, fall from heights, and auto accidents. Many injuries in fraternities also involve fatal and near-fatal falls from fraternity house roofs, windows, and sleeping porches. One common feature of these lawsuits is that they involved circumstances that are fueled by an excess of alcohol and an absence of supervision.

(Chart: http://www.theatlantic.com/features/archive/2014/02/the-dark-power-of-fraternities/357580/)

In February 2014, reports surfaced that a woman was raped at the Cornell University chapter house of Delta Upsilon. Just days later, the Penn State chapter of Delta Upsilon was criminally charged with furnishing alcohol to minors during a party that reportedly resulted in a female college student being sexually assaulted. In spite of that, the Penn State chapter of Delta Upsilon had recently reopened after being on probation for similar events. (http://www.collegian.psu.edu/news/crime_courts/article_4b6ded3a-afc6-11e3-9662-0017a43b2370.html) ; (http://www.centredaily.com/2014/03/24/4101351/penn-state-delta-upsilon-penalties.html) Despite claiming adherence to its founding principles, Delta Upsilon has found itself embattled in litigation for severe injuries and death of fraternity members across the United States.(http://www.campustimes.org/2012/12/06/bordeaux-family-files-24-million-lawsuit/) ; (http://tech.mit.edu/V134/N20/du.html)

Journalist Caitlin Flanagan immersed herself in the world of fraternities for a year. As Flanagan notes in The Dark Power of Fraternities, fraternities “have a long, dark history of violence against their own members and visitors to their houses, which makes them in many respects at odds with the core mission of college itself.” (http://www.theatlantic.com/features/archive/2014/02/the-dark-power-of-fraternities/357580/)

Private universities have the ability to restrict access to fraternities on their campuses, or have banned fraternities and sororities altogether. However, because the First Amendment to the U.S. Constitution guarantees freedom of assembly, public universities are prohibited from banning fraternities. But how can a fraternity continue to operate in light of the obvious risks of lawsuits for serious injuries that are both likely and preventable?

Fraternities and sororities are divided into numerous individual entities, with a national corporation headquartered in one state and smaller entities spread throughout the U.S. In many states, a local chapter cannot be sued because it lacks any status as a legal entity. Accordingly, when you sue the local chapter of a national institution, you are commonly suing an entity that has no legal status and owns no assets. Another tool to insulate fraternities from liability is to relinquish ownership in the fraternity house to a housing corporation. The housing corporation then leases the fraternity house back to the members of the chapter.

The Fraternal Information and Programming Group (FIPG) developed comprehensive risk-management guidelines. More than thirty fraternities are members of FIPG. According to FIPG, there are only two circumstances in which alcohol is ever permitted at fraternity social events. The first is through hiring a third-party vendor to check identification and sell and serve alcohol. The other permissible option is through the BYO policy, which requires that each guest (including fraternity members) bring only a limited number of alcoholic beverages. Although known to be an option to keep individuals safe, fraternities take few efforts to enforce these risk management guidelines.

Fraternities gain revenue by charging “loss prevention” dues to their members which insure themselves against catastrophic injuries. Rather than “loss prevention” policies, these are more aptly characterized as “loss response” policies because they provide insurance payments for the most tragic injuries that are bound to occur but do little to prevent the injury from occurring.

In the event that these injuries do occur, fraternities (and their insurers) frequently attempt to deny insurance coverage to the members of the fraternity because they act in a manner that violates the risk management policies that are inconsistent with the fraternity’s objectives. Oftentimes it is the fraternity member’s parents that are on the hook for these injuries. With substantial effort, time, and discovery, the national entity can be held liable for these injuries based upon their involvement and control over the local chapter.